One of the most important forces in the economy isn’t interest rates, inflation, or even unemployment. It’s liquidity. And right now, I don’t think enough people are paying attention to what’s happening with it.

The basic definition of liquidity is how quickly and easily something can be converted to cash without a significant loss in value. Cash itself is perfectly liquid. A house is illiquid. A publicly traded stock sits somewhere in between. When liquidity is strong, banks lend freely, deals get done, and asset prices generally rise. When it tightens, everything slows down. Financing gets harder to find. Borrowers face more scrutiny. And eventually, that pressure shows up in real estate, in business investment, and in the broader economy. I’ve been watching this for over 30 years, and the pattern is always the same. Think of liquidity as the oil in the engine of the economy. You can have a perfectly good engine, but without oil, it seizes up. That’s what we’re starting to see right now, and it matters enormously for anyone involved in real estate.

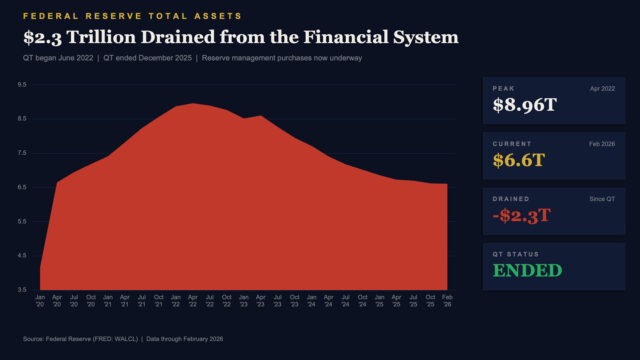

Here’s what’s happening beneath the surface. The Federal Reserve drained roughly $2.3 trillion from the financial system through quantitative tightening between mid-2022 and the end of 2025, shrinking its balance sheet from nearly $9 trillion down to around $6.6 trillion. (See the chart nearby). While QT officially ended in December 2025 and the Fed has begun small purchases of Treasury bills to maintain bank reserves, we’re still operating with far less liquidity than during the boom years. On top of that, the private credit market is showing real signs of stress. Just this past week, Blackstone saw record redemption requests of $3.8 billion from its flagship BCRED fund, about 7.9% of shares. BlackRock had to cap withdrawals from its $26 billion HPS lending fund after investors tried to withdraw 9.3% of the fund’s net asset value. And Blue Owl Capital permanently ended quarterly liquidity payments in one of its retail-facing funds. These are not small, obscure funds. These are the biggest names in private credit, and they are all dealing with investors who want their money back. When that happens, these funds have less capital available to make new loans, and a lot of that lending goes directly into commercial real estate.

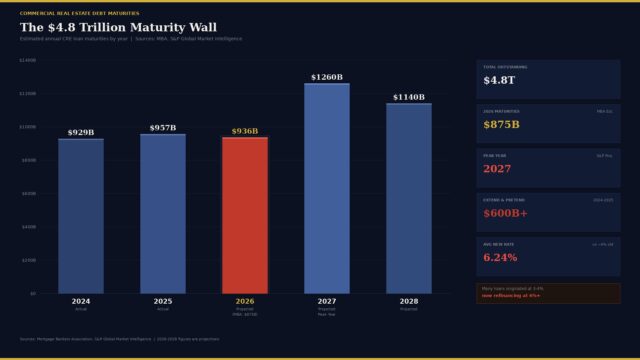

The real estate picture gets even more complicated when you look at the debt coming due. According to the Mortgage Bankers Association, approximately $875 billion in commercial and multifamily mortgage debt is scheduled to mature in 2026, with S&P Global projecting even larger waves in 2027 and 2028. Many of these loans were originated when interest rates were 3% to 4%. Today, the average new CRE loan rate is around 6.24%. That gap is enormous, and it means borrowers who need to refinance are facing much higher costs, tighter underwriting, and in many cases, they need to bring more equity to the table. A lot of lenders have been playing the “extend and pretend” game over the past two years, modifying and extending loans to avoid forced sales. But that strategy just pushed the problem forward. Those extended loans are now crowding into the 2026 and 2027 maturity windows, which is why the wall of debt coming due keeps growing. On March 3rd, the U.S. Treasury announced it’s pursuing a comprehensive review of bank liquidity rules, arguing that current regulations have limited banks’ ability to lend. That’s a meaningful signal, but regulatory changes take time, and the pressure on borrowers is here right now.

Here is what I always come back to in cycles like this. Liquidity tightening creates both challenges and opportunities. When financing gets harder, some borrowers face real stress. Distressed sales increase. Weaker operators get squeezed. But for investors with strong balance sheets and available capital, competition declines, asset prices become more attractive, and better deals start appearing. We saw this after the financial crisis in 2008 and 2009, and we are seeing the early stages of it again. Colliers is forecasting a 15% to 20% increase in CRE sales volume in 2026 as institutional capital re-enters the market to pick up opportunities. The key right now is to understand where you sit. If you’re overleveraged with loans coming due, this is the time to get ahead of it. If you have dry powder and a strong balance sheet, pay close attention, because the next 12 to 18 months could produce some of the best buying opportunities we’ve seen in years.