Thirty years. Roughly $2 billion in assets. About 10,000 apartment units across the western U.S. When someone with that kind of track record says a window is opening, it’s worth paying attention.

And right now, that window is open.

How we got here

In 2021, money was almost free. Mortgage rates sat below 3%, and operators were buying commercial real estate everywhere. An apartment building generating $450,000 a year in net income could carry a $10 million price tag and still cash flow comfortably.

Then inflation hit 9.1% in June 2022, and the Fed moved fast. Rates went from the floor to the ceiling in about 18 months.

Here’s the problem. A lot of that 2021 and 2022 buying was done with floating rate debt. Variable rate loans. Bridge loans. Short-term construction financing. When rates moved, the debt payments moved with them.

Same $10 million building. Same tenants. Same rents. One thing changed: annual debt service jumped from about $290,000 to $450,000. A property that produced $160,000 in annual cash flow is now losing money every month.

Multiply that by 100 units. 300 units. A whole portfolio.

What distress actually looks like

In Dallas alone, there are reportedly 1,000 multifamily buildings sitting at a debt service coverage ratio of 1.0 or below. That means 100% of net income goes to the lender, nothing left over. Lenders typically require a cushion of 1.25 to 1.30. At 1.0, you’re on a watch list.

It gets worse when a loan matures. If a building is now worth $6 million but the loan balance is $7 million, the equity is gone. The owner can’t refinance because no lender will issue a new loan exceeding the property’s value. The lender ends up taking the asset back.

Then, after getting appraisals and broker opinions, they start looking for buyers. Quietly. That’s when experienced operators step in.

Buying at 25 cents on the dollar

Consider a real deal from a few weeks ago: 278 units in San Antonio, built in 1979, 5% occupied. The instinct is that it must be in a terrible location.

It wasn’t. Solid B location. Owned by a lender who needed out.

Purchase price: $8 million. Roughly $28,000 a unit. The same property was appraised at $45 million in 2021 after a full renovation.

The plan: put another $20,000 to $30,000 per unit in, fully renovate, lease it up. Total all-in basis: around $16 to $20 million. On a property worth $45 million 3 years ago.

That’s what “25 cents on the dollar” actually looks like. And deals like this are out there right now.

Why the opportunity is bigger than just distress

We’re also roughly 4 million rental units short nationally.

After 2008, construction lending dried up for years. Builders stopped building. Millions of Americans lost homes and became renters. Demand spiked; supply didn’t keep up. That gap drove rents up for most of the 2010s.

The same setup is forming again. The wave of new deliveries from 2021 and 2022 is creating a temporary oversupply in some markets. But new starts have collapsed. When that delivery wave clears, very few units are coming behind it. Rent growth is coming. It’s just masked right now by concessions in overbuilt pockets.

There’s a useful illustration of this in Phoenix right now. Downtown properties are offering 3 to 4 months free on a 12-month lease just to land a tenant. Drive 5 miles to Tempe, near Arizona State, and there are no concessions and full occupancy. Same metro. Same moment. Completely different stories.

Where you buy matters more than when.

The maturity wall

Billions in commercial real estate loans are maturing over the next 2 to 3 years. These are real loans with real maturity dates at real banks, debt funds, and life insurance companies.

As those loans come due, lenders have 3 choices: extend and hope conditions improve, restructure, or take the property back and sell. More are choosing the third option, especially when loan balances exceed property values.

The original owner’s equity is already gone in many of these situations. The buyer’s conversation is with the lender, not the operator.

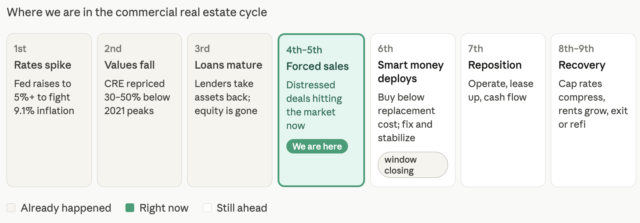

Where we are in the cycle

Think of it in innings.

We’re somewhere in the 4th or 5th inning. The first 3 already happened: rates spiked, values fell, loans started maturing. We’re now in the part of the cycle where forced sales are accelerating. That’s the inning when buyers with capital and real operating experience can step in at prices that make the math work.

The window is roughly 2 years. After that, distress gets absorbed, prices recover, and you’re competing with everyone else again on terms that don’t favor the buyer.

The investment thesis in plain terms

The filter is simple: can you buy a property, fix it, and get it to cash flow at today’s interest rates? If yes, buy. If no, pass.

No modeling a speculative exit cap rate. No betting on rate cuts. Underwrite to today’s numbers. If it works now, the up