Inflation has been the big story for 5 years. But something is quietly replacing it as the thing Americans are most worried about. Polls now show more people are afraid of losing their job than they are of rising prices. And that shift matters a lot more than most people realize.

Here’s the thing about inflation: it’s painful, but people keep spending. They cut corners, they swap brands, they grumble about the grocery bill. But they still feel okay going out to eat, booking a flight, keeping the lights on. Job insecurity? That hits different. When people don’t trust their paycheck, they freeze. They stop buying houses. They stop moving. They stop spending on anything they don’t absolutely have to.

We’re starting to see the early signs of that freeze right now.

The job market isn’t what the headlines say it is

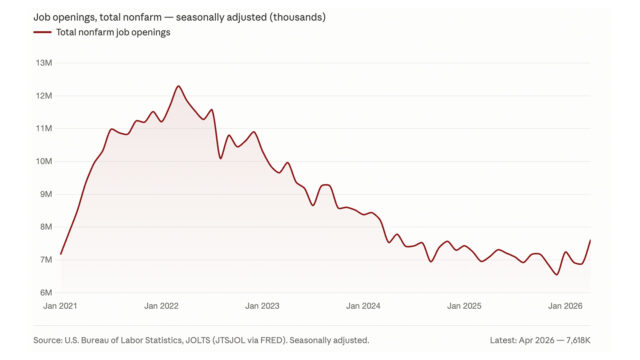

The official unemployment rate sits around 4.3%, which sounds fine. But look a little deeper and the picture changes. Back in 2022, there were about 12 million job openings in the U.S. Today there are roughly 7.4 million. That’s a 40% drop in active hiring. And the jobs that are still out there? They take a lot longer to land.

The average job search right now runs about 26 weeks. That’s nearly 6 months. So if you lose your job tomorrow and you think you’ll have something lined up in a few weeks, you probably need to reconsider that assumption. And if you don’t have 5 or 6 months of savings sitting around, that window gets really uncomfortable, really fast.

Here’s the part that makes this worse: savings rates have dropped to about 2.6%. Before the pandemic, they were hovering between 7 and 8%. So not only is it taking longer to find work, but the financial cushion most people would fall back on is almost gone.

AI is quietly gutting the white-collar workforce

When people talk about AI replacing jobs, they usually picture factory robots or fast food kiosks. But the jobs getting disrupted right now are office jobs. Accounting. HR. Marketing. Customer service. Middle management. The roles that built the American professional class.

Think about what’s happening inside almost any company right now. They’re asking: can AI do this task instead? And for a surprising number of tasks, the answer is yes. That doesn’t mean everybody gets fired tomorrow. But it does mean companies are hiring fewer people to fill those roles, and over time, departments are getting smaller.

Amazon recently cut 14,000 corporate jobs. Meta laid off 10% of its workforce. These aren’t seasonal positions or hourly roles. These are white-collar corporate jobs. And the companies doing it aren’t struggling financially. They’re doing it because they can do more with less, and AI is what made that possible.

Small businesses are going through the same thing. Owners are bringing in consultants, auditing their processes, and asking where automation can replace headcount. It’s happening across accounting, customer service, marketing, and HR. The businesses aren’t doing anything wrong. They’re just responding to what’s available.

What this means for real estate

If people are worried about their jobs, they’re not buying houses or looking to increase their costs with a move or a bigger apartment. Full stop.

People only make major financial moves when they feel stable. A mortgage is a 30-year commitment. Nobody signs that when they’re not sure they’ll have income next year. And lenders feel the same way: even if you’ve been unemployed and then land a new job, most lenders want to see 6 months to a year of steady income before they’ll approve you. So even when things improve, there’s a significant lag before the housing market actually feels it.

The flip side of that is renters. If fewer people are buying, more people are renting. That can be a tailwind for rental property owners. But there’s a catch. Renters are your customers. If their industry gets disrupted, if they’re out of work for 4 or 5 months burning through their savings, they may struggle to pay rent. You can’t separate the health of your rental portfolio from the health of the workforce filling your units.

Both things can be true at the same time: more demand for rentals and more risk from financially stressed tenants. Investors need to hold both of those realities at once rather than just seeing the demand side.

The broader picture

Something interesting is happening with the data itself. The official job numbers come out, and then get revised. And revised again. In 2024, the annual revision knocked 818,000 jobs off the previous count. Nobody made a big deal out of it. But that’s not a rounding error. That’s a significant difference in how the economy actually looks versus how it was reported.

The people who are living this don’t need a government report to tell them something feels off. They know people who have been job hunting for months. They see 500 to 1,000 applicants competing for the same post online. That’s the real signal.

Credit card balances are up. Savings are down. Job openings have fallen nearly 40% from their peak. AI is quietly restructuring entire job categories. And the average job search is now a 6-month ordeal for people who often don’t have 6 months of cushion to work with.

Inflation was the story of the last 5 years. The job market might be the story of the next 5. And for real estate investors and everyday Americans alike, it’s worth paying close attention to how this plays out.