Most people nod along and sign. They don’t really know what those words mean in practice, until something goes wrong.

Right now, something is going wrong. Across the country, deals that were financed in 2021 and 2022 at ultra-low interest rates are hitting a wall. Lenders are finally foreclosing. Values are down 30-40% in some markets. I’ve personally looked at properties in Texas with less than 10% occupancy.

So this is the right time to understand the capital stack. Because where you sit in it determines whether you get paid, or lose everything.

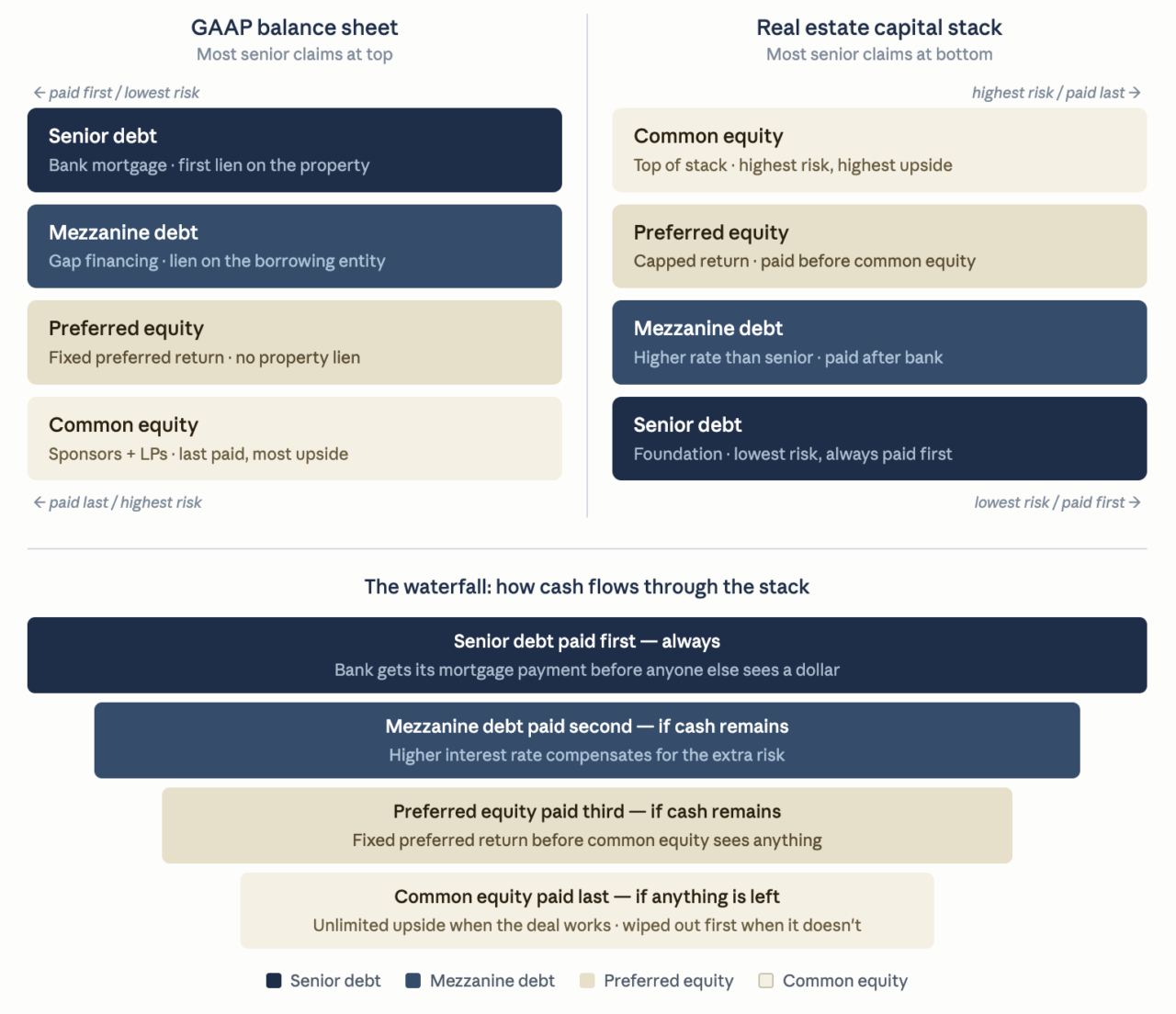

Think of it like a building. Every real estate deal is funded by multiple sources of money stacked on top of each other. There are 4 layers.

Let’s walk through each one.

This is the mortgage. A bank or institutional lender puts up the largest chunk of money, typically 50-65% of the total cost of the deal, and they get the best legal protections in return.

If the deal goes sideways and the property has to be sold or foreclosed, the bank gets paid first. Before anyone else sees a dime.

They also hold a lien directly on the property itself. That’s a legal claim that says: if you don’t pay me, I can take the building. It’s recorded in the county courthouse. It’s real.

Because of that protection, the bank takes the least risk. And because they take the least risk, they accept the lowest return, usually somewhere in the 5-7% range depending on market conditions.

What this means for you as an LP: You are not the bank. The bank will get paid even if you don’t.

Sometimes a deal needs more money than the bank will lend, but the sponsor doesn’t want to give up more equity. That’s where mezzanine debt comes in. It fills the gap between what the bank lends and what the equity investors put in, typically 10-20% of the total deal cost.

Mezzanine lenders don’t hold a lien directly on the property like the bank does. Instead, they take an ownership interest in the entity that owns the building. It’s a step removed, which means they carry more risk than the bank.

Because of that extra risk, they charge higher interest rates, often in the 10-14% range. And if the deal defaults, the mezzanine lender gets paid only after the bank is made whole.

Mezzanine debt isn’t in every deal. You’ll see it more often in larger, more complex transactions or in development projects.

This is where many LP investors land, and it’s worth understanding carefully.

Preferred equity sits above mezzanine debt in the stack, which means it carries more risk than either form of debt. But it sits below common equity, meaning preferred equity investors get paid before the sponsor and other common equity holders do.

Preferred equity investors are technically owners of the deal, not lenders. But they don’t have a lien on the building the way a bank does. Their protection is contractual: they have a legal right to receive a fixed preferred return (often 6-10%) before any profits flow down to common equity.

If certain defaults occur, preferred equity holders may have the right to take management and ownership control of the entity that owns the underlying real estate from common equity holders, in many cases completely wiping out the common equity holders’ value in the transaction.

That’s the teeth behind preferred equity. It’s not as strong as a bank lien, but it’s not nothing.

The trade-off: preferred equity investors typically don’t share in the upside if the deal does really well. They get their fixed return and that’s it. The potential for big gains goes to common equity.

This is where the sponsors live, and often where a large portion of LP investors sit as well.

Common equity is the last to get paid. If the deal produces cash flow, everyone below common equity gets their cut first. Whatever is left flows up to common equity holders through what’s called a waterfall distribution.

Picture cash flowing through the capital stack like water cascading down a series of pools. Senior debt fills first, then mezzanine debt, then preferred equity, and finally common equity. Only after each pool is full does water flow to the next level. In lean times, the lower pools may never fill at all.

That’s the honest picture. In a bad year, the bank gets paid. The mezzanine lender gets paid. The preferred equity investors get paid. And common equity gets whatever’s left. Which could be nothing.

But here’s the flip side: when the deal works, common equity has unlimited upside. When a property doubles in value and gets sold, the bank doesn’t share in that. The preferred equity investors don’t share in that either. The gain flows up to common equity.

More risk. More potential reward.

You’ll see the capital structure presented two ways depending on the context. On a formal balance sheet, senior debt sits at the top because it’s the highest-priority claim. In real estate deal decks, investor presentations, and capital raising materials, the same structure gets flipped: senior debt moves to the bottom as the foundation everything else rests on. Same information, two different visual conventions. Both are correct.

Here’s why I wanted to write this piece today, not five years ago.

We’re in the middle of a CRE debt crisis. Thousands of deals done in 2021 and 2022 used floating-rate bridge loans at near-zero interest rates. Those rates went from roughly 3% to 7% or higher when the Fed raised rates aggressively in 2022-2023. A $10,000 monthly mortgage payment became $20,000. Deals that made sense stopped making sense overnight.

And now those loans are maturing. Lenders who spent years extending and pretending are finally taking properties back. Values are down 30-40% in many markets. A deal bought at $100 million might be worth $50 million today, less than the loan balance.

When that happens, the capital stack tells the story of who survives.

The bank: gets paid first. Usually okay. The mezzanine lender: might get paid partially, might get wiped. The preferred equity: in serious trouble. The common equity: likely gone.

This is not hypothetical. We have watched this play out in real time on deals across Texas, Arizona, and the Southeast. Unfortunately the investors who got hurt worst were the LPs, the ones sitting in common equity, in deals with floating rates and where the cash flow couldn’t cover once rates doubled.

Before you write a check into any deal, ask these questions:

1. Where am I in the capital stack? Are you common equity? Preferred equity? What’s above you? What’s below you?

2. What’s the loan-to-value ratio? If a property is worth $10 million and the debt is $8 million, there’s very little cushion for equity investors if values drop.

3. Is the debt fixed or floating? Floating rate debt was the killer in the last cycle. If the sponsor has a floating rate bridge loan with no rate cap, that’s a red flag right now.

4. What’s the preferred return threshold? If you’re in preferred equity, what exactly triggers your return? Is it “hard” (you get paid regardless of cash flow) or “soft” (only if the property generates enough income)?

5. What does the waterfall look like? Ask the sponsor to walk you through the distribution waterfall in plain English. How much does the property need to earn before you see money? How does a sale get split?

The capital stack is not a technicality. It’s the legal and financial architecture of every deal you invest in. It determines your rights, your return expectations, and your exposure if things go wrong.

Lower in the stack: safer, slower money. Higher in the stack: riskier, but with more upside.

Right now, with lenders foreclosing on distressed assets all over the country, understanding where you sit has never been more important. The people who didn’t understand the capital stack in 2021 are the ones getting the hard lesson today.