When President Trump recently floated the idea of a 50-year mortgage, most people laughed at first. But according to multiple reports, this proposal is highly probable, and if it happens, it will fundamentally change how Americans buy homes.

Let’s unpack what this means for buyers, renters, and real estate investors.

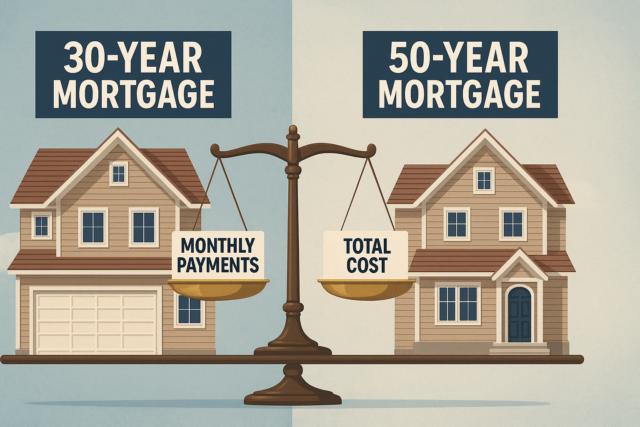

Lower Payments, Not Cheaper Homes

At its core, the 50-year mortgage is designed to lower monthly payments, not housing prices. It’s similar to how car loans evolved — once limited to 36 months, now stretching to 84 months or longer.

If the average U.S. home costs about $415,000, with 20% down and a 6.2% interest rate, the monthly payment on a 30-year mortgage is roughly $2,034. A 50-year mortgage could bring that down to around $1,700.

That $300 difference sounds small, but across millions of buyers, it’s massive. It opens the door to ownership for those previously priced out, and it also pushes demand even higher.

A Modern “New Deal”

When Franklin Roosevelt introduced the 30-year mortgage during the New Deal, critics called it insane. Now, Trump may be crafting his own “New Deal” extending the loan term to 50 years.

If history repeats itself, home prices will rise. Why? Because people buy homes based on their monthly payment, not the total cost. Lower payments mean buyers can qualify for larger loans, which means prices inevitably adjust upward.

Who Wins and Who Loses

If the 50-year mortgage becomes reality, there will be clear winners and losers.

Winners:

-

First-time homebuyers who’ve been stuck renting because monthly payments were out of reach.

-

Sellers, who’ll suddenly find more buyers able to afford their homes.

-

Existing investors, whose properties could appreciate as affordability expands.

Losers:

-

Renters, as monthly mortgage payments begin to rival national rent averages (around $1,600).

-

Future buyers, who’ll face higher home prices as demand surges.

-

Apartment owners like me — because the gap between renting and owning will shrink fast.

Could It Create a Bubble?

Make no mistake, this move could heat up the market fast. The U.S. already faces a housing shortage of 4–7 million units. With supply tight and payments dropping, prices will likely accelerate.

But that doesn’t automatically mean a crash is coming. The difference this time is that underwriting standards remain stricter than they were during the 2008 financial crisis. So while it might create a new “limit” on pricing, it doesn’t necessarily create a bubble that bursts, just one that expands.

What About Investors?

One of the biggest questions: Will this apply to investors?

If it does, it could open up a flood of leveraged capital chasing deals, and potentially destabilize the market. Personally, I hope the 50-year option is limited to first-time homebuyers. America needs more people building equity, not more institutional buyers competing with families for starter homes.

Long-Term Implications

Beyond affordability, the 50-year mortgage could unfreeze the housing market. Right now, roughly 80% of homeowners hold mortgages under 4%, which keeps them from selling. By extending loan terms, homeowners could sell and buy again without doubling their payment.

It also helps fix one of America’s biggest problems, trapped equity. There’s over $34 trillion in home equity across the country, nearly as much as the entire U.S. stock market. The 50-year mortgage could unlock some of that capital and get it moving again.

The Generational Divide

Older generations often scoff at the idea of a 50-year mortgage:

“Why would anyone want to be in debt for 50 years?”

But younger buyers see it differently. For a couple in their 20s or 30s, a 50-year term could mean finally getting into a home they can afford, a fixed housing cost instead of rising rent.

The truth is, the average age of a first-time homebuyer is now over 40 years old. Just a decade ago, it was 28. That alone shows how affordability has shifted — and why this proposal exists in the first place.

Final Thoughts: A Turning Point for Real Estate

If Trump’s 50-year mortgage becomes law, it will reshape real estate for decades.

It could create new homeowners, boost GDP, and unlock trillions in equity, but it could also inflate prices and squeeze renters even more.

Like any major policy change, it’s neither purely good nor bad. The key is to understand how it shifts incentives, and position yourself on the right side of that shift.

For first-time buyers, this could be a golden window.

For investors, it’s time to prepare for a new wave of demand, and the price growth that comes with it.

Ready to Learn the System?

Inside KenPro, I teach the frameworks, strategies, and real-world lessons I wish I had when I began. If you are serious about building wealth, ownership, and long-term independence through real estate, this is where your journey begins.