The Fed can’t cut when prices keep rising. But high inflation has its own way of pushing property values up. Either way, the case for real assets holds.

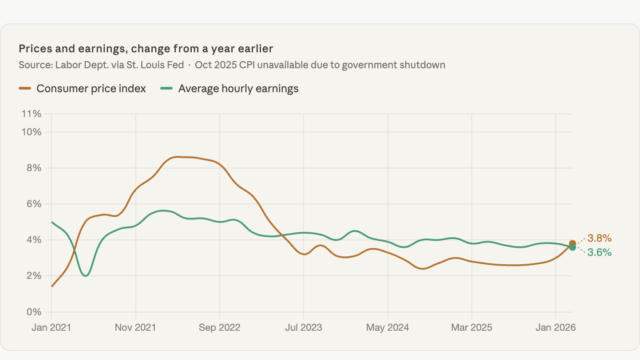

The April CPI came in at 3.8% year-over-year, and markets noticed. Bond investors expects higher inflation. That’s the market saying it doesn’t believe inflation is going quietly. And as long as that’s true, the Federal Reserve has very little room to cut: the Fed won’t loosen policy until it’s confident inflation is sustainably back at 2%. At 3.8%, they’re not there.

The labor market complicates this further. Which we covered in this podcast April’s jobs report showed 115,000 jobs added, stronger than expected on the surface. But look underneath and the picture softens considerably. Government and healthcare are doing the heavy lifting. Private-sector hiring is slowing. White-collar layoffs continue in tech, finance, and media. The household survey, which measures actual employment rather than payrolls, has been weaker than the headline number for months. That’s not the kind of labor data that forces the Fed’s hand toward cuts. So rates stay elevated, and long-term mortgage rates follow.

“Two part-time jobs replacing one full-time job still counts as job growth.”

For real estate, the direct math is straightforward: higher rates mean higher borrowing costs, which suppress transaction volume, compress cap rates, and keep would-be buyers sitting on the sidelines. The lock-in effect compounds this. Homeowners who locked in 3% mortgages in 2020 and 2021 aren’t selling into a 7% world. Inventory stays low, affordability stays broken, and the market stays frozen. That’s the rate story. But the inflation story runs in the other direction. Real assets, historically, absorb inflation. Rents tend to rise alongside prices. Replacement costs go up as construction materials and labor get more expensive, which puts a floor under existing property values. The asset itself becomes harder to replicate, and therefore more valuable in nominal terms.

The interesting thing about this moment is that both roads may lead to the same place for long-term real estate holders. If rates come down, transaction volume recovers and valuations rise as capital floods back in. If rates stay elevated but inflation persists, real estate does what it has always done during inflationary periods: it holds, and often appreciates, in dollar terms. The consumer stress is real. Credit card debt is at a record $1.3 trillion. Subprime auto delinquencies are at 30-year highs. The K-shaped economy is no longer just an abstraction. But for investors positioned in well-located, cash-flowing real assets, the macro case right now is stronger than the headlines suggest, not weaker.