Somewhere in Dallas right now, there are nearly 1,000 multifamily properties where 100% of net operating income goes straight to debt service. Not profit. Not reserves. Not investor distributions. Just keeping the loan alive.

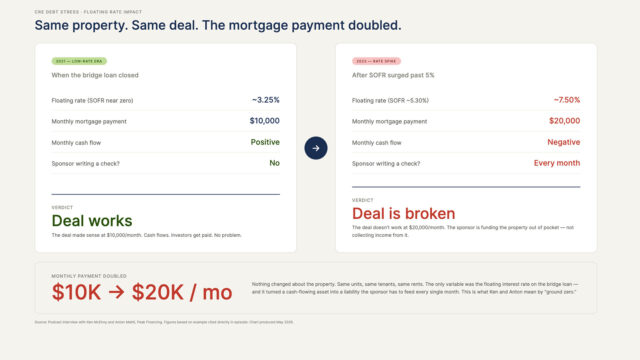

And in most cases, the property itself is fine. Occupancy is stable. Rents are being collected. The operator is doing exactly what the business plan said to do. The only thing that changed was the interest rate on a floating-rate bridge loan, and it turned a cash-flowing asset into a liability the owner has to fund out of pocket every single month.

I sat down recently with Anton Mattli from PeakFinancing.com to talk through what he’s seeing on the ground. He’s a commercial real estate lender watching this play out in real time, and his view is that what’s happening behind the scenes is significantly worse than what’s being reported.

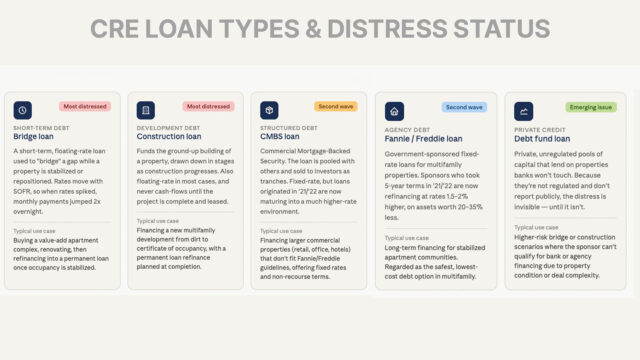

Ground zero isn’t everywhere. It’s concentrated in bridge loans and construction loans originated in 2021 and 2022, when SOFR was sitting near zero and floating-rate debt was almost free. When the Fed moved 500 basis points in 18 months, those loans repriced overnight. A $10,000 monthly mortgage payment became $20,000. Same property. Same tenants. Same rents. The math just stopped working. Owners who were collecting cash flow are now writing checks to keep the doors open.

The scale is hard to see from the outside, and that’s partly structural. Lenders have been quietly extending, deferring interest, and kicking the can rather than foreclosing, partly because they lack the asset management infrastructure to take these properties back, and partly because foreclosing forces them to mark the actual loss on their books. Private debt funds make the picture murkier. Because they’re unregulated and don’t report publicly, distress doesn’t aggregate anywhere. There’s no number to point at. But behind the scenes, across every major market, hundreds of loans are sitting in limbo. Lenders know what they have. Sponsors are out of cash. And the properties, in some cases, have deferred maintenance in the 8 figures that nobody has written down yet.

The lesson for investors watching this unfold is blunt: buy for cash flow today, not for what a property might be worth later. Fix the rate. Underwrite to today’s cap rates, or slightly higher. If the 10-year Treasury drops toward 3.5%, that’s the signal to refinance. But don’t build a business plan around it. The 2021-2022 playbook of assuming rates would stay low and valuations would keep climbing is precisely what created this mess. The water has been rising for two years. At some point, the dam breaks.

Check out the full discussion here.