For years, real estate investors focused on the usual drivers of returns: rent growth, occupancy, financing costs, and property appreciation. Insurance was often treated as a predictable operating expense—a line item that rarely received much attention during underwriting. That assumption no longer holds true.

In 2026, insurance costs have become one of the fastest-growing expenses affecting both homeowners and real estate investors. Across the country, premiums are rising at a pace that is forcing investors to rethink deal assumptions, reassess market risk, and place greater emphasis on operational efficiency. While rising interest rates have dominated headlines over the past few years, insurance may quietly be becoming one of the most significant threats to property-level profitability.

Insurance Has Moved From a Minor Expense to a Major Variable

Historically, investors could forecast insurance costs with reasonable confidence. Small annual increases were expected and easily absorbed through rent growth or operational improvements. Today’s environment is different.

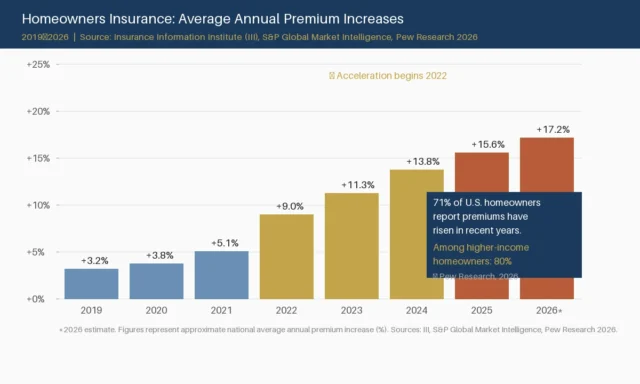

A 2026 Pew Research survey found that 71% of U.S. homeowners report that their homeowners insurance costs have increased in recent years. Among higher-income homeowners, that number rises to 80%. The overwhelming majority of homeowners now view rising insurance expenses as a growing financial burden.

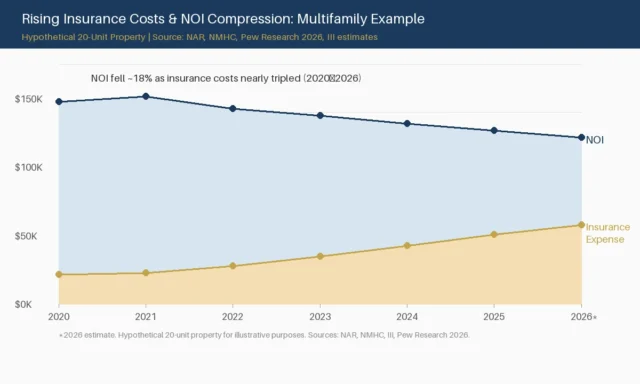

What makes this trend particularly important for investors is that insurance costs directly impact Net Operating Income (NOI). Every dollar spent on insurance is a dollar that no longer contributes to cash flow. In multifamily investing, where property values are largely based on income, rising insurance expenses can reduce valuations even if rents remain stable.

Why Premiums Are Rising Across the Country

Insurance companies are facing pressures from multiple directions simultaneously. The cost of repairing and rebuilding homes has increased significantly due to inflation in labor, materials, and construction services. At the same time, insurers are dealing with larger claim payouts resulting from extreme weather events and natural disasters.

According to Pew Research data, homeowners identify rising repair and rebuilding costs as one of the primary reasons behind higher premiums. Many also cite increased insurance company costs associated with weather-related losses.

The challenge is not limited to coastal markets or traditional disaster zones. Flood risk, wildfire exposure, severe storms, and other climate-related events are influencing underwriting decisions across a growing number of states. Nearly all U.S. counties have experienced some form of flooding since the mid-1990s, and updated risk models continue to reshape how insurers evaluate exposure.

The Impact on Real Estate Investors Is Larger Than Many Realize

For investors, rising insurance costs create a double challenge.

First, they increase operating expenses immediately. A property that was underwritten two or three years ago may now face substantially higher premiums than originally projected. This compresses cash flow and reduces investor distributions.

Second, insurance inflation can affect future acquisition decisions. Properties located in areas with elevated climate risk may become less attractive as operating expenses continue to rise. Investors are increasingly evaluating not just location and demographics, but also insurability and long-term insurance trends.

In some markets, insurance costs are growing faster than rental income. When that happens, the traditional strategy of relying on rent growth to offset expense increases becomes much more difficult.

Insurance Is Becoming a Market Selection Factor

For decades, investors evaluated markets based on population growth, job creation, landlord-friendly regulations, and housing demand. Insurance costs are now emerging as another critical variable.

A market with strong rent growth may appear attractive on the surface, but if insurance expenses are increasing at an unsustainable rate, long-term returns can suffer. Similarly, properties in regions vulnerable to hurricanes, wildfires, or flooding may face higher operating costs regardless of occupancy performance.

This does not mean investors should avoid these markets entirely. It simply means insurance must become part of the underwriting conversation from the beginning.

The best investors are increasingly stress-testing deals using higher insurance assumptions rather than relying solely on historical costs.

What Investors Can Actually Do About It

The good news is that rising insurance costs are not completely outside an investor’s control.

Industry experts consistently recommend reviewing coverage annually rather than automatically renewing existing policies. Shopping multiple carriers, bundling policies, and reassessing coverage limits can often uncover savings opportunities.

Property improvements can also help reduce premiums. Security systems, fire protection upgrades, impact-resistant roofing, and other risk-mitigation measures may qualify for discounts depending on the insurer. Some insurers offer meaningful reductions for properties that demonstrate lower claim risk.

Another strategy involves evaluating deductibles carefully. Higher deductibles can reduce annual premiums, though investors must ensure they have adequate reserves to absorb potential claims.

Ultimately, the goal is not simply finding the cheapest policy. The goal is balancing cost, coverage quality, and long-term protection.

The Bigger Risk Is Underestimating the Trend

Perhaps the greatest mistake investors can make is assuming that insurance costs will return to historical patterns. While annual increases may moderate in some regions, most industry observers expect insurance to remain a larger operating expense than it was a decade ago.

This shift has important implications for underwriting. Deals that appear attractive using outdated insurance assumptions may produce disappointing results in practice. Investors who build conservative insurance projections into their models are likely to be better positioned than those relying on historical averages.

Real estate investing has always been about understanding risk before it becomes obvious. Insurance is increasingly becoming one of those risks.

The Bottom Line

Rising insurance costs are no longer just a homeowner problem—they are an investor problem. What was once a routine operating expense has become a meaningful driver of profitability, valuation, and market selection. As premiums continue to climb across much of the country, investors who treat insurance as a strategic consideration rather than a minor line item will have a significant advantage.

In real estate, returns are often determined by the expenses investors fail to anticipate. In 2026, insurance may be the most important one.