For the last several years, real estate investors, homebuyers, and economists have all focused on one question: when mortgage rates finally come down, will housing demand return?

The conventional wisdom has been straightforward. Higher rates reduced affordability, sidelined buyers, and slowed transaction activity. Therefore, lower rates should naturally bring demand back into the market. But recent housing data suggests the relationship may not be that simple.

Despite mortgage rates recently falling to their lowest levels in over a month, homebuyer activity remains surprisingly weak. Purchase mortgage applications have declined, refinancing activity has softened, and transaction volumes continue to lag historical norms. The data highlights an important reality for investors: mortgage rates are only one piece of a much larger housing affordability equation.

Housing Demand Depends on More Than Interest Rates

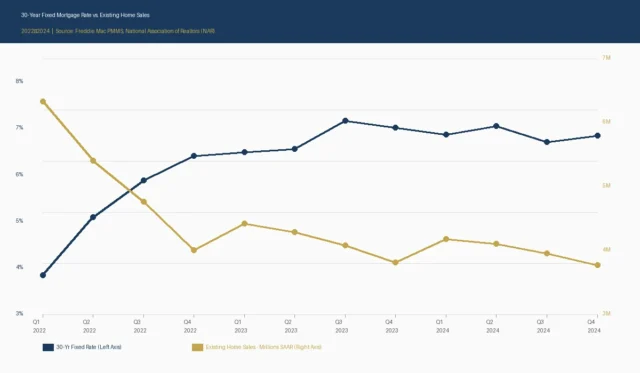

For much of the post-pandemic housing cycle, mortgage rates became the primary explanation for market conditions. As rates climbed above 7%, affordability deteriorated rapidly, causing many buyers to pause their home search.

However, even as rates have moved lower in recent weeks, buyer activity has not responded as many expected.

This disconnect reveals something important. Buyers are not simply reacting to financing costs. They are evaluating the entire financial commitment associated with homeownership, including home prices, insurance costs, property taxes, maintenance expenses, and broader economic uncertainty.

When affordability remains stretched across multiple variables, modest declines in mortgage rates may not be enough to significantly change buyer behavior.

Affordability Remains the Market’s Biggest Challenge

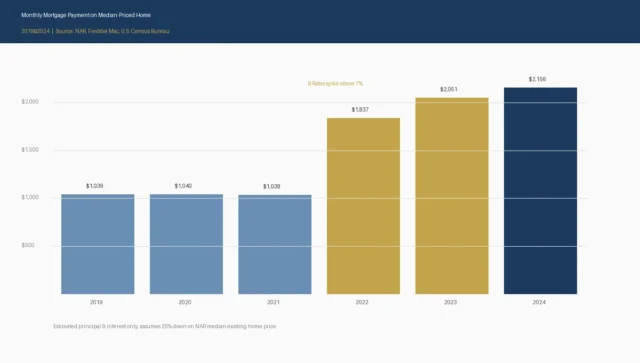

One of the most significant issues facing the housing market today is that home prices have remained elevated despite slower sales activity.

Historically, declining demand would often lead to meaningful price corrections. This cycle has been different. A combination of limited inventory, demographic demand, and homeowners locked into low-rate mortgages has prevented widespread price declines.

As a result, many prospective buyers face a difficult situation. While mortgage rates may be lower than recent highs, monthly housing payments remain substantially higher than they were just a few years ago.

For many households, affordability is still the primary barrier to entry.

This dynamic explains why demand has remained relatively muted even as financing conditions improve.

Inventory Is Improving, But Not Enough

The housing market has seen some inventory growth compared to the extremely constrained conditions of 2021 and 2022. More listings are appearing in many markets, and buyers generally have more options than they did during the peak frenzy years.

However, inventory remains below long-term historical averages in many regions.

The challenge is that the supply that is entering the market is often concentrated in specific price segments or geographic areas. Entry-level inventory remains limited in many markets, leaving first-time buyers with fewer affordable options.

This imbalance continues to restrict transaction activity and limits the impact that lower mortgage rates might otherwise have on demand.

Economic Uncertainty Is Influencing Buyer Behavior

Housing decisions are rarely based solely on interest rates. They are deeply connected to consumer confidence and economic expectations.

Many buyers remain uncertain about inflation, employment conditions, and the broader economic outlook. Even when mortgage rates improve, uncertainty about future financial stability can discourage large purchases.

This is particularly relevant after several years of elevated inflation and changing monetary policy. Consumers who feel uncertain about future expenses are often more cautious about taking on long-term mortgage obligations.

For investors, this highlights an important principle: confidence drives housing demand just as much as affordability.

What This Means for Real Estate Investors

For real estate investors, the current environment reinforces the importance of focusing on fundamentals rather than waiting for a single catalyst.

Many investors assumed that lower rates would immediately reignite transaction activity and drive another wave of appreciation. The recent data suggests the recovery may be more gradual.

Instead of relying on mortgage rate movements alone, investors should pay attention to broader market indicators such as:

- Household formation

- Employment growth

- Population migration

- Wage growth

- Housing supply trends

- Consumer confidence

These factors often have a more durable impact on long-term housing demand than short-term fluctuations in financing costs.

Investors who focus exclusively on interest rates risk missing the larger forces shaping the market.

The Market Is Returning to Normal

One of the most overlooked aspects of today’s housing market is that slower activity does not necessarily indicate weakness. In many ways, the market is simply moving back toward historical norms after an unusually volatile period.

The housing boom of 2020 through 2022 was driven by extraordinary circumstances, including record-low interest rates, pandemic-related migration patterns, and unprecedented levels of liquidity.

Those conditions were unlikely to last forever.

What investors are seeing now may be less about a housing slowdown and more about a normalization process. Transaction volumes, buyer behavior, and pricing dynamics are gradually returning to levels that resemble traditional housing cycles.

For long-term investors, that is not necessarily bad news. Stable, predictable markets often create better investment opportunities than highly speculative ones.

Looking Beyond Mortgage Rates

Mortgage rates will continue to influence housing demand, but they are no longer the only story.

Affordability challenges, inventory constraints, rising operating costs, and economic uncertainty are all playing important roles in shaping buyer behavior. As a result, lower rates alone may not be enough to unlock significant demand in the near term.

The investors who perform best in this environment will be those who look beyond headline rate movements and focus on underlying fundamentals. Real estate has always been driven by supply, demand, and demographics. Those forces matter just as much today as they ever have.

Mortgage rates may be falling, but the housing market is reminding investors that sustainable demand requires more than cheaper financing. It requires affordability, confidence, and strong economic fundamentals. Until those factors align more closely, housing demand is likely to remain more subdued than many expected.