The Federal Reserve made headlines this week, and not because they cut rates. In fact, they didn’t cut anything. But what happened at Chairman Kevin Warsh’s first Fed meeting on Wednesday may be one of the most important shifts in how America’s central bank operates in over a decade. The message was clear: the rules of the game are changing, and most people are still playing by the old ones.

What the Fed Actually Did

The Federal Open Market Committee voted unanimously to hold interest rates right where they’ve been, between 3.5% and 3.75%. That part wasn’t a surprise. What was surprising was just about everything else.

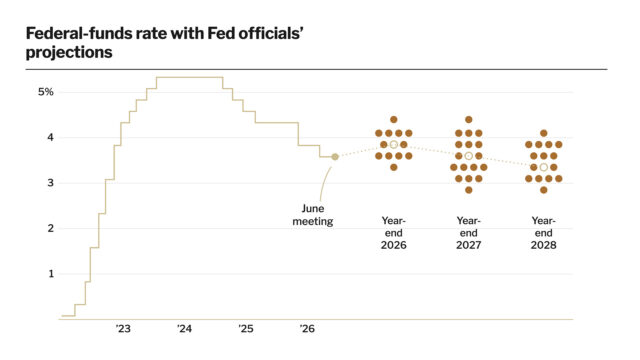

Nearby is a chart showing historical and projected Fed funds rates. The chart uses the “dot-plot” for the projection. The dot-plot is an estimate from each member of the committee as to where future rates will land.

The biggest story wasn’t the rate decision itself. It was the dramatic shift in where Fed officials think rates are headed. Back in March, 12 out of 19 Fed officials expected at least one rate cut by the end of 2026. Nobody expected a rate hike. Fast forward to this week, and that picture has completely flipped. Now nine officials expect at least one rate increase by year’s end. Only one still thinks a cut is coming. Eight expect no change at all.

In other words, the Fed has gone from “we’re probably cutting” to “we might actually be raising” in just three months.

What caused this dramatic U-turn? Two big things: the war with Iran, which sent oil prices surging and pushed overall inflation to a three-year high, and a labor market that refused to weaken the way many experts predicted. Add in the economic boom driven by artificial intelligence spending, and the Fed finds itself dealing with an economy that is running hotter than expected.

Who Is Kevin Warsh And Why Does It Matter?

Kevin Warsh is President Trump’s pick to lead the Fed, and he came in with a very clear agenda. He wants the Fed to talk less, do more, and stop trying to predict the future out loud. That philosophy showed up immediately at his first press conference.

The Fed’s policy statement this week was only 132 words long. The April statement was 246 words. Warsh stripped out language that used to tell markets what the Fed might do next, what’s known as “forward guidance.” His message was simple: we’re not going to telegraph our next move anymore.

He also did something unusual. He didn’t even submit his own dot, the forecast that each official provides showing where they think rates will be in the coming years. The “dot plot” this week had 18 submissions instead of the usual 19. Warsh has argued that these projections actually limit the Fed’s ability to change course when the economy shifts, so he sat this one out.

Warsh also announced four task forces to review how the Fed communicates, manages its massive $6.7 trillion balance sheet, uses economic data, and thinks about jobs and productivity. These aren’t just internal housekeeping moves. They signal that Warsh is planning to reshape how the central bank functions from the ground up.

The Inflation Problem Isn’t Going Away

Here’s the part that matters most to everyday investors and homeowners: inflation is still a serious problem.

Fed officials now expect overall inflation to end 2026 at 3.6%, and core inflation (which strips out food and energy) at 3.3%. The Fed’s target is 2%. That gap is a big deal, and Warsh made it clear in his press conference that getting back to 2% is the mission — no exceptions.

Energy prices are a major driver. Oil above $90 a barrel means higher costs for transportation, shipping, food, and just about everything else. Those costs don’t disappear overnight, even if the war ends tomorrow. Companies pass higher shipping and fuel costs directly to consumers, and those price increases take time to work their way back down.

The AI boom is adding fuel to the fire as well. The massive build-out of data centers across the country is pouring spending into the economy. More spending, more demand, higher prices. What many thought would eventually lower prices is actually pushing them up in the short term.

What This Means for Real Estate Investors

Too many people are using the fed funds rate as an excuse to sit on the sidelines. And that strategy has a real cost, even if that cost is invisible.

Right now, conditions in multifamily real estate look a lot like 2007 to 2009. Cap rates are up, expenses are up, occupancy is softer, and values are down in many markets. For long-term investors, that kind of environment is often where real buying opportunities show up.

Inflation is part of the equation, always has been, always will be. If you’re holding cash while inflation runs at 3.6%, you’re losing purchasing power every single day. Getting into a hard asset that moves with inflation, real estate, gold, productive farmland, is how regular people have built generational wealth for decades. Ken’s own mother, a hairdresser, bought a house for $10,700. That house is now worth $700,000. She didn’t time the market. She just got in and stayed in.

The Bottom Line

The Warsh Fed is a different animal than what investors have grown used to. Expect fewer hints about what’s coming next. Expect more surprises. And expect that the Fed will be laser-focused on fighting inflation, even if that means rates go up before they come down.

For investors, the takeaway is this: stop waiting for the Fed to save the day with rate cuts. That story has changed. Focus instead on understanding the current cycle, protecting your purchasing power, and making educated moves toward assets that can weather an extended higher-rate, higher-inflation environment.

The cost of doing nothing is real. It just doesn’t show up on a statement.

Ken McElroy is a real estate entrepreneur, educator, and author. He hosts The Ken McElroy Show and the annual Limitless conference. This post is for educational purposes only and is not financial or investment advice.